As the world becomes increasingly interconnected, cross-border financial transactions form the backbone of global commerce. The SWIFT payments/banking system serves as the lifeline for secure and efficient international money movement.

What is SWIFT?

SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, is a secure messaging network facilitating global financial transactions among over 11,000 institutions in more than 200 countries. Founded in 1973 by 239 banks from 15 countries, SWIFT’s primary aim is to ensure smooth, standardized, and secure cross-border communication between financial institutions.

SWIFT does not transfer money itself but facilitates the transmission of payment instructions, making international banking faster, more secure, and less error-prone.

Before SWIFT, banks relied on the TELEX system, a cumbersome and error-prone method of international communication. The lack of standardization made financial transactions slow and insecure. By 1977, SWIFT had replaced TELEX as the preferred method of interbank communication, ensuring efficiency and security. Today, SWIFT facilitates millions of messages daily, with recent reports indicating an average of 44.8 million messages processed per day.

What is the SWIFT Payment System?

A SWIFT transfer involves sending electronic payment instructions across borders. Although SWIFT does not handle funds, it ensures secure transmission of transaction details such as the recipient’s account information and transfer amount.

Key Components of SWIFT Transfers

- BIC codes: These are unique codes that identify financial institutions in the SWIFT network.

- SWIFT messages: The messages are in standardized formats for payment instructions, ensuring accuracy and consistency.

- Nostro and Vostro accounts: Nostro accounts hold foreign currency in another bank, while Vostro accounts represent foreign funds held domestically.

Role of Intermediary Banks

Intermediary or correspondent banks facilitate transactions between banks without a direct relationship. These banks ensure seamless processing but may increase transaction costs and processing times.

How Does a SWIFT Payment Work?

Here’s a step-by-step overview:

- Initiation: The sending bank creates a SWIFT message containing recipient details, account information, and transfer amount.

- BIC codes: Institutions involved are identified using their unique Bank Identifier Codes.

- Message transmission: SWIFT securely transmits the payment message.

- Processing: The recipient’s bank verifies the details and processes the transaction via Nostro and Vostro accounts.

How to Make a SWIFT Transaction?

- Collect the required information:

- Recipient’s name, address, account details, routing code

- Recipient’s bank SWIFT code

- Reason for the transfer

- Additional documentation as requested by your bank

- Initiate transfer:

- Log in to your bank’s online platform or visit a branch

- Complete the SWIFT transfer form

- Confirm and pay fees:

- Review all details and pay associated fees.

- Track transfer:

- Retain the transaction receipt to monitor the progress of the transfer.

Example of SWIFT Payment

A business in India imports machinery from a supplier in Japan. The Indian company instructs its bank to make a payment to the Japanese supplier’s bank. The Indian bank generates a SWIFT message containing all the transaction details, including the supplier’s account number and bank SWIFT code. This message is transmitted securely through the SWIFT network. Upon receipt, the Japanese bank credits the supplier’s account and adjusts the necessary Nostro and Vostro accounts. This streamlined communication ensures that the payment is accurate and efficient despite the geographical distance.

What are the Fees for SWIFT Transfers?

SWIFT transfer fees vary depending on:

- Transaction amount: Higher amounts may have lower percentage fees.

- Currency conversion: Transactions involving exotic currencies may incur higher costs.

- Intermediary banks: Each additional bank involved increases the overall fees.

- Typical fees include:

- Sending bank: $25-$50

- Intermediary banks: $10-$50

- Exchange rate markup: 2-3%

Who Uses SWIFT Payments?

SWIFT is essential for a wide range of financial activities, including:

- Financial institutions: Banks and credit unions use SWIFT for cross-border payments and settlements.

- Corporations: Multinational companies rely on SWIFT for treasury management and trade finance.

- Investment firms: These firms use SWIFT for securities trading and fund transfers.

Individuals indirectly benefit from SWIFT through their banks.

Transferring Time for SWIFT Payments

SWIFT transactions typically take 2-5 business days, depending on national holidays, the number of intermediary banks, and the accuracy of transaction details.

Is BIC the Same as a SWIFT Code?

Yes, BIC (Bank Identifier Code) and SWIFT codes are essentially the same. They are unique identifiers used to direct payments to the correct financial institutions globally.

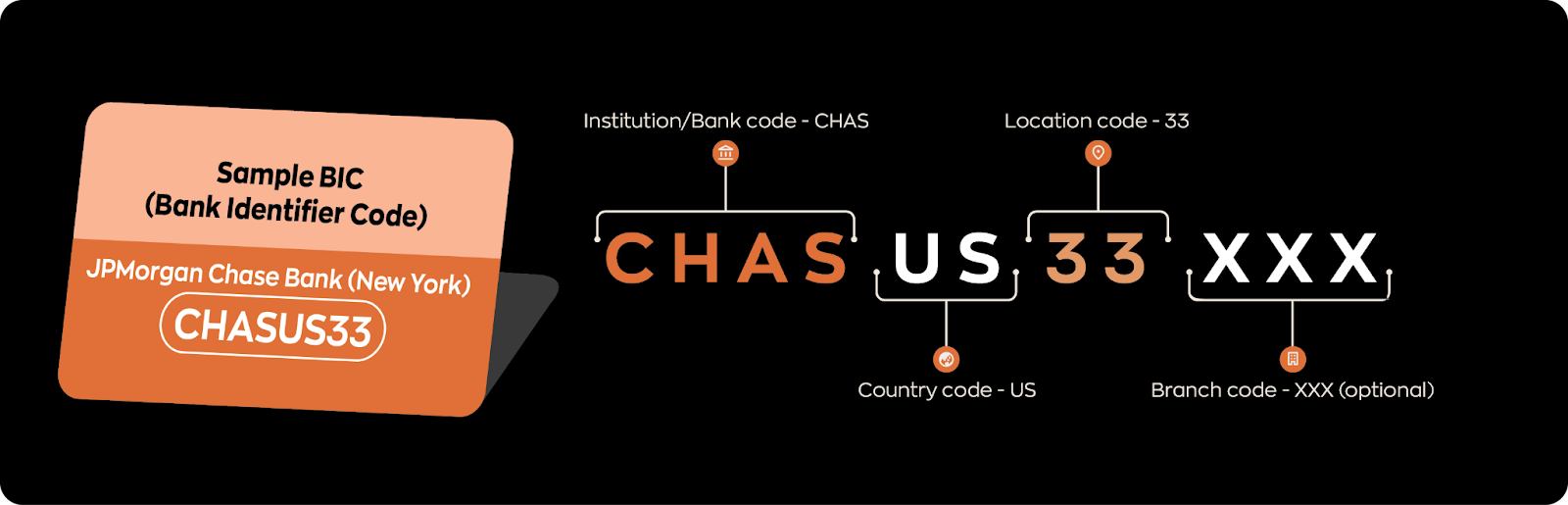

Sample BIC (Bank Identifier Code)

JPMorgan Chase Bank in New York has the BIC code CHASUS33.

- First four characters: Institution/Bank code (CHAS for JPMorgan Chase Bank)

- Next two characters: Country code (US for the United States)

- Next two characters: Location code (33 for New York)

- Last three characters (optional): Specific branch identifier

Importance of SWIFT in Global Finance

SWIFT underpins global trade and finance by:

- Facilitating international payments: It provides a reliable platform for seamless cross-border transactions.

- Supporting trade finance: It standardizes communication for letters of credit and guarantees.

- Enabling securities transactions: It ensures secure messaging for trades and settlements.

Who Owns the SWIFT Banking System?

SWIFT is a member-owned cooperative governed by its shareholders, primarily financial institutions. Its neutrality ensures fair access for all participants.

Common Issues and Challenges with SWIFT

- High costs: Multiple fees, including those from intermediary banks, can be expensive.

- Processing Delays: Errors or holidays can extend processing times.

- Security Risks: Constant vigilance is required to combat cyber threats.

- Emerging Competition: Blockchain and fintech alternatives are gaining traction.

FAQs

What is SWIFT in banking?

SWIFT is a secure global messaging network for financial transactions.

How do I send a SWIFT payment?

To send a SWIFT payment, gather the recipient’s name, bank account details, and SWIFT code. Then, initiate the transfer through your bank’s online platform or by visiting a branch.

Is SWIFT pay safe?

Yes, SWIFT payments are considered highly secure due to their encryption protocols and authentication processes.

How long does a SWIFT transfer take?

SWIFT transfers typically take 2-5 business days to process. Delays may occur due to errors, holidays, or additional checks by intermediary banks.

How to find a SWIFT code?

You can find your bank’s SWIFT code by:

- Checking your bank statement.

- Logging into your bank’s online banking platform.

- Contact your bank’s customer service.

- Visit your bank’s official website, where SWIFT codes are often listed under the ‘Contact’ or ‘International Banking’ sections.

0 Comments